Gold and oil are very different in their investment characteristics since gold is purchased principally to hold as an inflation hedge and oil is purchased primarily for refinement into gasoline and other petroleum products. Typically, this makes oil much more subject to international political factors and global economic forces. However, Gold has taken a more prominent role over the last few years as it has become a de-facto ‘anchor’ currency that is value-constant against monetary fluctuations by central banks.

Gold and oil are very different in their investment characteristics since gold is purchased principally to hold as an inflation hedge and oil is purchased primarily for refinement into gasoline and other petroleum products. Typically, this makes oil much more subject to international political factors and global economic forces. However, Gold has taken a more prominent role over the last few years as it has become a de-facto ‘anchor’ currency that is value-constant against monetary fluctuations by central banks.

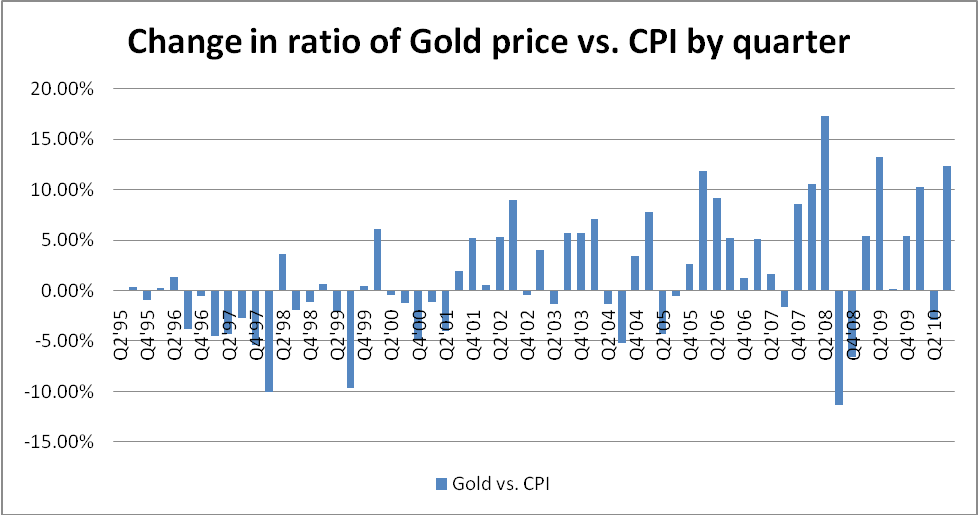

During the 1990’s, Gold prices did not even hold pace with the Consumer Price Index as market sentiment was tilted more toward stocks and the business sector. After the terrorist attacks of September 11th, gold regained some of its prominence, but it was the financial crisis of 2008 that brought Gold into the forefront. Over the last few years, gold prices have appreciated significantly faster than the CPI. This reflects a market sentiment that is anticipating large amounts of future inflation, and is seeking Gold as a place to hold value when paper currencies de-value.

In the 2010 forecast book, we forecasted a gold price of $1,211 by the end of the year. By the month of November, Gold has surpassed that price to close at $1,368. The most recent surge in gold prices has come from announcements of more quantitative easing by the Federal Reserve.

Because of continued quantitative easing, we expect to see the price of gold finish 2011 at $1,601 per ounce, reflecting a continued desire on the part of investors for a hedge against inflation. There is also a risk of steep price contraction with gold if economic fundamental stabilize more quickly than previously anticipated.

Another factor influencing price volatility for gold is the fact that it is not a production commodity and does not generate earnings or dividends. Since the value of gold is primarily driven by its speculative value to other investors, there is the potential for dramatic price swings if market sentiment experiences any abrupt changes. Historical economic cycles have seen price spikes in gold that rapidly retreated when investor confidence in the economy restored. Our estimate for 2011 is that the moderating effect of mid-term elections will help to stabilize political forces, but that a return to economic expansion will not transpire until after the year elapses.

The Solomon Success Team

![]()

Flickr / Mykl Roventine