One of the most important concepts for investors to understand is that a dollar today is not the same as a dollar yesterday, and is not the same as a dollar tomorrow. Over time, inflation erodes the purchasing power of currency. This is critically important, because most people focus on the nominal change in the value of their investments, but unintentionally ignore their real value after accounting for past and expected future inflation.

One of the most important concepts for investors to understand is that a dollar today is not the same as a dollar yesterday, and is not the same as a dollar tomorrow. Over time, inflation erodes the purchasing power of currency. This is critically important, because most people focus on the nominal change in the value of their investments, but unintentionally ignore their real value after accounting for past and expected future inflation.

The most significant factor that impacts prices is the supply of money relative to economic output. While it is true that the prices of individual items relative to one another will fluctuate in the marketplace, the only thing that can drive the price of everything up at once or everything down at once is an increase or decrease in the supply of money chasing after goods or services. It is important to note that “money” can take the form of currency, bank deposits, or lines of credit.

Bearing the cause of inflation in mind, it is also important to understand how the government measures inflation. The most commonly cited measurement of inflation is the consumer price index.1 This index is expressed as a bundle of consumer goods, and is intended to represent the likely purchasing behavior for an urban household. (Over time, the household size assumption for CPI has been decreasing, meaning that when the consumer bundle is expressed in a per-person instead of per-household basis, the increase is faster than expressed in CPI) The index value derives from comparing the consumer bundle price to the bundle price in the base year(s).

As time goes by, the items in the government consumer bundle are changed to reflect shifts in purchasing behavior. In addition to this, quality changes are imputed into the index so that an item that costs the same, but has greater quality shows up as having a lower cost in the consumer bundle. There are many other adjustments made to CPI, but in aggregate, they make objective pricing comparisons from one time period to another difficult since there are many subjective adjustments that have gone into computation of the index.

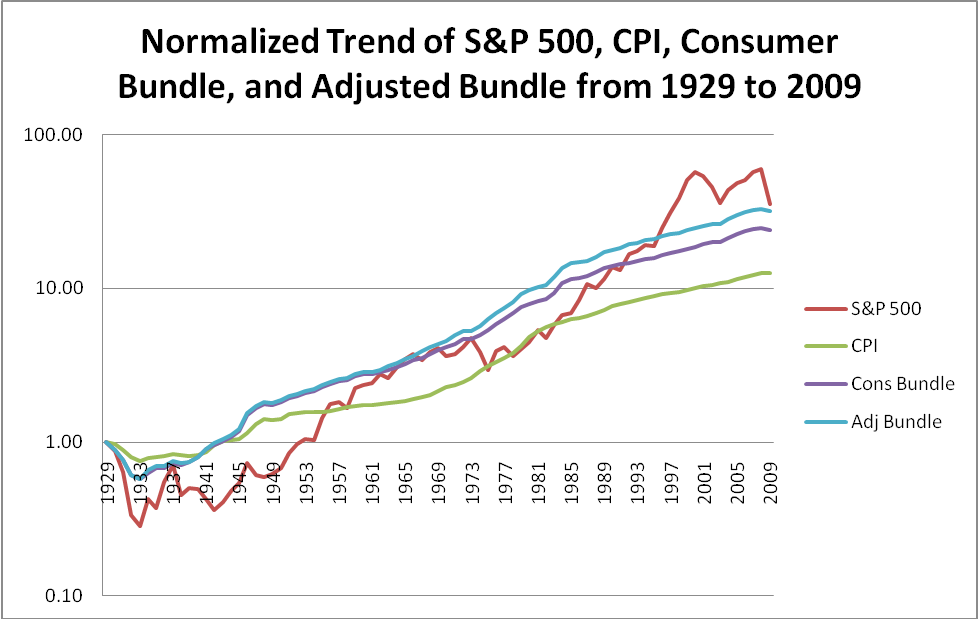

As a way of level-setting the value of CPI, we have constructed a comparison of the relative values2 for the S&P 500 stock market index, the consumer price index, the consumer product bundle3, and the consumer product bundle normalized for per-person instead of per-household from 1929 through 2009. Analysis of the trending shows provides some very interesting insights for investors.

As a way of level-setting the value of CPI, we have constructed a comparison of the relative values2 for the S&P 500 stock market index, the consumer price index, the consumer product bundle3, and the consumer product bundle normalized for per-person instead of per-household from 1929 through 2009. Analysis of the trending shows provides some very interesting insights for investors.

The first is that over time, the CPI and CPI bundle diverge very significantly. Presumably, this is due to price adjustments for quality improvements of CPI component items. However, it also shows that the nominal increase in price of items over time is likely to be larger than what is expressed in the CPI. Another interesting insight is the fact that the adjusted bundle tracks very closely with the consumer bundle until the 1960’s. This is the point when divorce rates began to increase and the average household size started shrinking. When the consumer bundle is spread across a smaller household size, it results in a higher cost per person than is expressed in the ‘per household’ assumption of the index.

Further analysis of the data trending shows that the S&P 500 significantly under-performed the CPI through the mid 1950’s, and basically held flat with CPI during the mid to late 1970’s. It wasn’t until the bull market of the 1980’s that the S&P 500 value really began to separate from CPI.4 After the financial crisis of 2008 drove down market values, the normalized value for the S&P 500 and the normalized value of the adjusted consumer bundle stood relatively close to one another.

This analysis provides a unique insight. Depending on how one defines inflation (CPI, Consumer Bundle, Adjusted Bundle), the long-term returns from the S&P 500 index become relegated mostly to dividends. For stock market investors who were caught in the value growth explosion of the technology and financial bubbles, it is important to understand that the rates of growth experience during those time periods are unlikely to be repeated anytime soon.

However, all investors must come to understand that nominal gains and real gains are very different things. The government assesses tax liabilities based on nominal gains, but as investors, we principally care about the ‘real’ rate of return generated by our investments. This means that we must seek investment vehicles that will produce ‘real’ rates of return in excess of future inflation.

Our preferred strategy for accomplishing this goal is with income properties. By purchasing an income-producing asset with fixed-rate financing, it allows investors to benefit from nominal value inflation since their cost of financing is fixed. Furthermore, by outsourcing the payment of mortgage interest to tenants who are paying rent, it allows income property owners the luxury of holding through value disruptions so that nominal price inflation helps them to create real wealth.

Financial independence is closer than you think. Buy your Early Bird ticket to the Meet the Masters of Income Property Investing educational event before February 14 to qualify for a steep discount on tickets.

The Solomon Success Show

![]()

Flickr / MoneyBlogNews