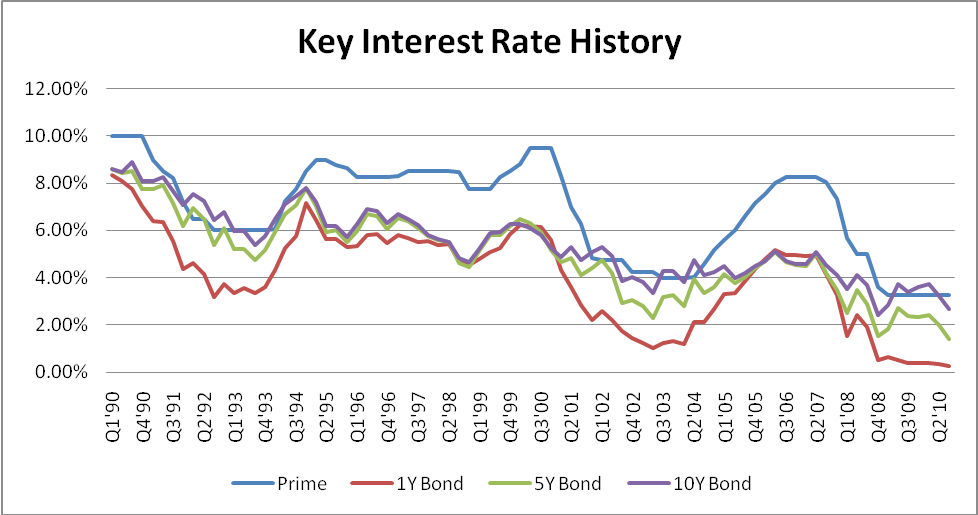

One of the principal economic leading indicators for 2011 will be the movement of 10-year treasury rates. The reason for this is because 30-year fixed rate mortgages are indexed against the 10-year treasury, and interest rate movements have a dramatic impact on the affordability of homes.

One of the principal economic leading indicators for 2011 will be the movement of 10-year treasury rates. The reason for this is because 30-year fixed rate mortgages are indexed against the 10-year treasury, and interest rate movements have a dramatic impact on the affordability of homes.

One of the significant problems faced by the government is the increasing difficulty in auctioning off treasury securities. The reason for this is investor fears over inflation and the relative low interest rate offered on the debt. These fears are amplified by the massive budget deficits being run by the Federal Government that must be financed with consistently increasing levels of borrowing. The strategy currently employed by the government is to use the Federal Reserve to purchase treasuries.

By adding treasury securities to the Federal Reserve balance sheet, the Fed is increasing the amount of banking reserves in the system that are available to be loaned out. Thus, every dollar in monetary expansion by the Fed can be turned into ten dollars by the banks through issuing loans under the 10% reserve requirement. Currently, this has not happened because of the near-zero interest rates being charged for loans from the Federal Reserve. Instead of loaning out these additional reserves, banks are using the funds to purchase treasuries and generate a profit on the interest rate spread. When the tide of new money creation eventually crashes in, it will result in a sudden upward surge in prices that will influence demand for treasury yields.

In the 2010 forecast book, we anticipated that rates would exit 2011 at 6.7% for a 10-year government bond. This estimate was based on the assumption that current levels of monetary expansion could not be continued indefinitely without adverse effect. As of November 2010, the 10-year treasury rate stood at 2.5%, supported by heavy purchases on the part of banks who are investing funds borrowed from the Federal Reserve at near-zero rates. Because of these factors, we believe that the 10-year treasury rate will finish 2011 at 5.75%. Our models have been adjusted to factor-in the spillover effects of quantitative easing pushing up yields demanded by investors in response to escalating consumer prices.

In the 2010 forecast book, we anticipated that rates would exit 2011 at 6.7% for a 10-year government bond. This estimate was based on the assumption that current levels of monetary expansion could not be continued indefinitely without adverse effect. As of November 2010, the 10-year treasury rate stood at 2.5%, supported by heavy purchases on the part of banks who are investing funds borrowed from the Federal Reserve at near-zero rates. Because of these factors, we believe that the 10-year treasury rate will finish 2011 at 5.75%. Our models have been adjusted to factor-in the spillover effects of quantitative easing pushing up yields demanded by investors in response to escalating consumer prices.

With current mortgage rates at historic lows, it is likely that the housing recovery will stall in the second half of the year as the interest rate increases erode affordability. For homeowners and investors that have capitalized on the current low interest rates, there is a significant probability that future inflation rates will be considerably higher than the current treasury and mortgage rates.

Financial independence is closer than you think. Buy your ticket to the March 4 – 6, 2011, Meet the Masters of Income Property Investing educational event before it sells out.

The Solomon Success Team

![]()

Flickr / RambergMediaImages

We’re not here today to ponder the merits of whether your Christian investment is green enough, but rather to consider the reality of what the recent recession has done to the so-called

We’re not here today to ponder the merits of whether your Christian investment is green enough, but rather to consider the reality of what the recent recession has done to the so-called